What is a VCC?

A Variable Capital Company (VCC) is an alternative form of corporate vehicle that will soon become available for Collective Investment Schemes (CIS). Presently, the organisational structures available to CIS are the company, limited partnerships, and the unit trust structures. The VCC can be used for both open-ended and closed-ended alternative and traditional fund strategies. As a corporate vehicle with flexible capital, shares are created when investments are made, and the shares are readily redeemable by the shareholders. This kind of flexibility was lacking in the existing vehicle of corporations available under The Companies Act that has several restrictions when it comes to capital reduction and dividend distribution. This new vehicle, exclusively designed for the fund management industry, will strengthen Singapore’s position as a fund management hub in the region.

Related Article: Setting up a fund management »Background of Variable Capital Company

The idea of the new flexible investment fund structure was first floated in 2016 at the Investment Management Association of Singapore’s annual conference. Later in March 2017, the Monetary Authority of Singapore issued a public consultation to seek feedback on the various aspects of this new Variable Capital Company corporate structure. The Ministry of Finance announced in the 2018 Singapore Budget Statement that a VCC would be treated as a company and a single entity for tax purposes. On 10 September 2018, a draft bill for the VCC was presented for the first reading in the parliament, and the bill was subsequently passed in the parliament on 1 October 2018. The VCC Act will come into effect in 2019, and the date is yet to be notified. The VCC framework incorporates several key features of open-ended/flexible capital vehicles that are already available in jurisdictions such as Luxembourg, Ireland, the UK, and the USA.

Originally named as Open-End Investment Company (OEIC), it came to be known as Singapore Variable Capital Company (“S-VACC”). Now, it has been renamed again, as the Variable Capital Company.

What Are the Features of the Variable Capital Company (VCC)?

The newly proposed structure has gathered a lot of interest in the fund management industry because of its unique features that will render operational flexibility to fund managers in Singapore. The following are key features of a VCC:

- It will be governed by the Variable Capital Companies Act (the Act). The Accounting and Corporate Regulatory Authority is the regulatory authority for the establishment and administrative purposes, and the Monetary Authority of Singapore (MAS) will oversee its anti-money laundering and countering the financing of terrorism obligations. The Securities and Futures Act will govern the offering of shares in a VCC and all other aspects concerning the VCC as a fund.

- VCC can be used for both traditional funds and alternative funds and can be used for retail investors or for restricted class investors.

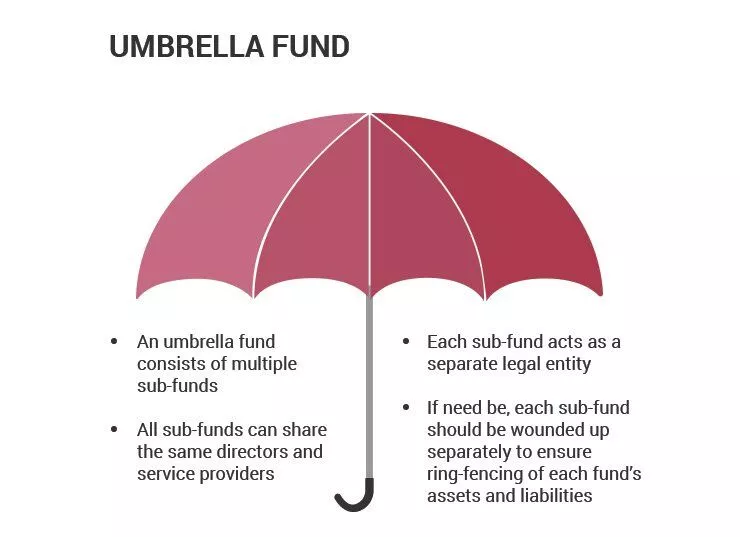

- It can be used as a standalone fund, or an umbrella entity with multiple sub-funds that may have different investment objectives, investors as well as assets and liabilities.

- Shares are redeemable without shareholders’ approval, and dividends are payable from the capital thus offering greater flexibility than corporations.

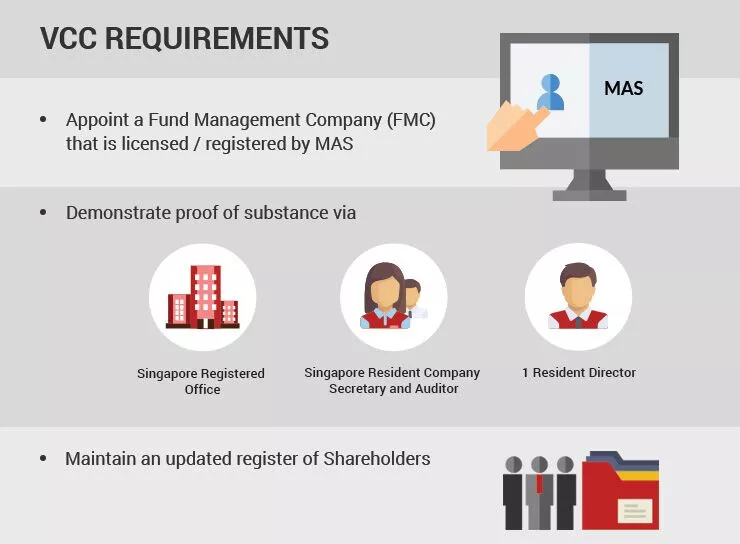

- It must appoint a fund management company (“FMC”) that is licensed or registered by MAS, or is an exempt financial institution in Singapore; this is to ensure substance as well as to prevent the misuse of the vehicle for unlawful purposes.

- Proof of substance must be demonstrated via a Singapore registered office, a Singapore resident company secretary and auditor, and at least one resident director;

- It must maintain an updated register of shareholders and disclose the information to the regulatory and law enforcement authorities upon request.

- VCCs offered to restricted investors (like accredited investors) can adopt various prescribed internationally accepted accounting standards like US GAAP, ASC Standard or IFRS.

What Are the Advantages of the Variable Capital Company (VCC)?

There is no need for solvency tests and corporate resolutions for issue and redemption of shares. Relief from such conditions ensures seamless movement of capital. Shareholders have greater freedom and flexibility to enter and exit a fund through easy subscription and redemption of shares. Such fluidity and flexibility are very critical for the efficiency of investment funds.

Typically, when funds are capitalised with redeemable preferred shares, the financial reporting standards require such instruments to be classified as liabilities, and this poses a problem at the time of solvency tests before capital reduction or redemption. Since VCCs are exempted from the solvency test, the limitation posed by the classification requirement of the reporting standard is obviated.

Unlike corporations set up under the Companies Act that requires dividends to be distributed from the profits only, VCCs can distribute dividends from the capital itself.

Although VCCs are required to maintain a register of shareholders, they need not disclose the register publicly.

The VCCs are allowed to be constituted as umbrella funds with several sub-funds that have different investment objectives, investors, and asset classes. Furthermore, the sub-funds could share a board of directors and have the same fund manager, custodian, auditor and administrative agent. Additionally, administrative functions could also be consolidated into the sharing of service providers, and administrative functions would pave the way for economies of scale and cost advantage.

The VCC framework allows for inward re-domiciliation, therefore funds structured as VCCs in other jurisdictions can easily re-domicile in Singapore, to tap into the Asian markets without losing their identity and legacy.

Furthermore, VCCs will enjoy the tax incentives and treatments that are available to current investment funds that are domiciled in Singapore. Subject to conditions, the Financial Sector Incentive extended to fund management companies and GST remission for funds will also apply to the VCCs.

Key Considerations for the Singapore Variable Capital Company:

The sub-funds under an umbrella structure do not have a separate legal identity. To address a potential contagion risk, whereby the assets and liabilities of the sub-funds get mixed up with or used to discharge the liabilities of other sub-fund, the VCC Act requires assets and liabilities of each sub-fund to be segregated. Each sub-fund must be wound up separately to uphold the segregation, and the winding up of one Sub-fund does not lead to the winding up of the VCC. As the sub-funds lack legal persona, the VCC may sue or be sued in respect of a sub-fund. A sub-fund of a VCC may invest in another sub-fund of the VCC.

Since the Act allows inward re-domiciliation of foreign-domiciled funds, many of the funds that used overseas jurisdictions to route investment via vehicles similar to VCC can now consider to re-domicile in Singapore and consolidate their pooling and investment activities. Those foreign-domiciled funds that are constituted as corporations will have to first convert to a VCC before re-domiciling in Singapore; alternatively, they can freshly incorporate a VCC in Singapore.

Related Read: How to Incorporate a VCC company in Singapore »Although shares can be issued and redeemed without shareholders’ approval, shares can be issued and redeemed only within the net asset value. This is to protect the creditors. However, for listed close-ended funds, this has to be in accordance with the relevant listing requirements.

The VCCs offered to retail investors must have at least three directors, including at least one independent director. A prospectus must also be filed with the MAS before offering shares, and the MAS must approve the VCC. An approved trustee must be appointed as the custodian of the VCC assets.

In its present form, the Act’s provisions relating to the insolvency of VCC has been adopted from The Companies Act. However, this would soon be amended with provisions from the Insolvency Bill along with appropriate modifications that are specific to VCC.

Related read: How the Variable Capital Company (VCC) is a global gamechanger after launch in Jan 2020 »Conclusion

The VCC is a new corporate vehicle that obviates the limitations of the existing structures. With this addition, Singapore’s position as the fund management hub is anticipated to become holistic and efficient with world-class management capabilities, robust regulatory framework and favourable tax regime. With the introduction of the VCC, the sector will witness a surge in activity with plenty of growth opportunity for service providers such as auditors, tax professionals, custodians, fund managers and advocates Singapore’s latest innovation for the fund management sector is a testimony for the city-states resolve to stay ahead of the competition to fortify its reputation as a pro-business asset and fund management hub in the region.

What You Need to Set Up a VCC

Frequently Asked Questions

What is a variable capital company VCC in Singapore?

- A Variable Capital Company (VCC) in Singapore is a flexible corporate structure designed for investment funds. It allows for the segregation of assets and liabilities across sub-funds while operating under a single legal entity. The VCC structure supports both open-ended and closed-ended fund strategies and benefits from tax exemptions under Singapore’s fund tax incentive schemes. It is regulated by the Accounting and Corporate Regulatory Authority (ACRA) and the Monetary Authority of Singapore (MAS).

How does a variable capital company work?

- A Variable Capital Company (VCC) in Singapore is a flexible corporate structure designed for investment funds. It allows for variable share capital, meaning shares can be issued and redeemed without shareholder approval, making it suitable for open-ended or closed-ended fund strategies. A VCC can operate as a standalone fund or as an umbrella fund with multiple sub-funds under one legal entity, enabling cost and operational efficiencies. It must be managed by a licensed fund manager and comply with regulatory requirements set by the Monetary Authority of Singapore (MAS).

What is the difference between VCC and SPV?

- A Variable Capital Company (VCC) is a corporate structure in Singapore designed specifically for investment funds, allowing for multiple sub-funds under a single legal entity with variable share capital. A Special Purpose Vehicle (SPV), on the other hand, is a subsidiary created for isolating financial risk or holding specific assets, commonly used in structured finance and securitization. While VCCs are regulated by the Monetary Authority of Singapore (MAS) and cater to fund managers, SPVs are general-purpose entities that may be set up as private limited companies and are not restricted to fund-related activities.

What does VCC mean in finance?

- In finance, VCC commonly stands for "Variable Capital Company." It is a type of corporate structure that allows for flexible capital and is often used for investment funds. While widely associated with Singapore’s fund management industry, the term may vary in meaning depending on jurisdiction.