When policy wobbles, markets move: what Harvard’s latest research signals for APAC boards

A new Harvard Business School analysis offers a useful datapoint for leaders watching the shifting politics of climate policy: nearly half of U.S. publicly listed companies in climate-relevant industries now disclose that they are developing “climate solutions.” In 2023 SEC filings, 49.6% of these firms reported work on climate-related technologies and products, up from 45% in 2022 and 20% in 2005.What’s striking isn’t just the trend line; it’s the timing. The research suggests that corporate investment in climate solutions has continued even as government support has become less predictable. In other words, while policy remains an important accelerator, the underlying driver increasingly looks like competitive strategy.

What the research did (and why it matters)

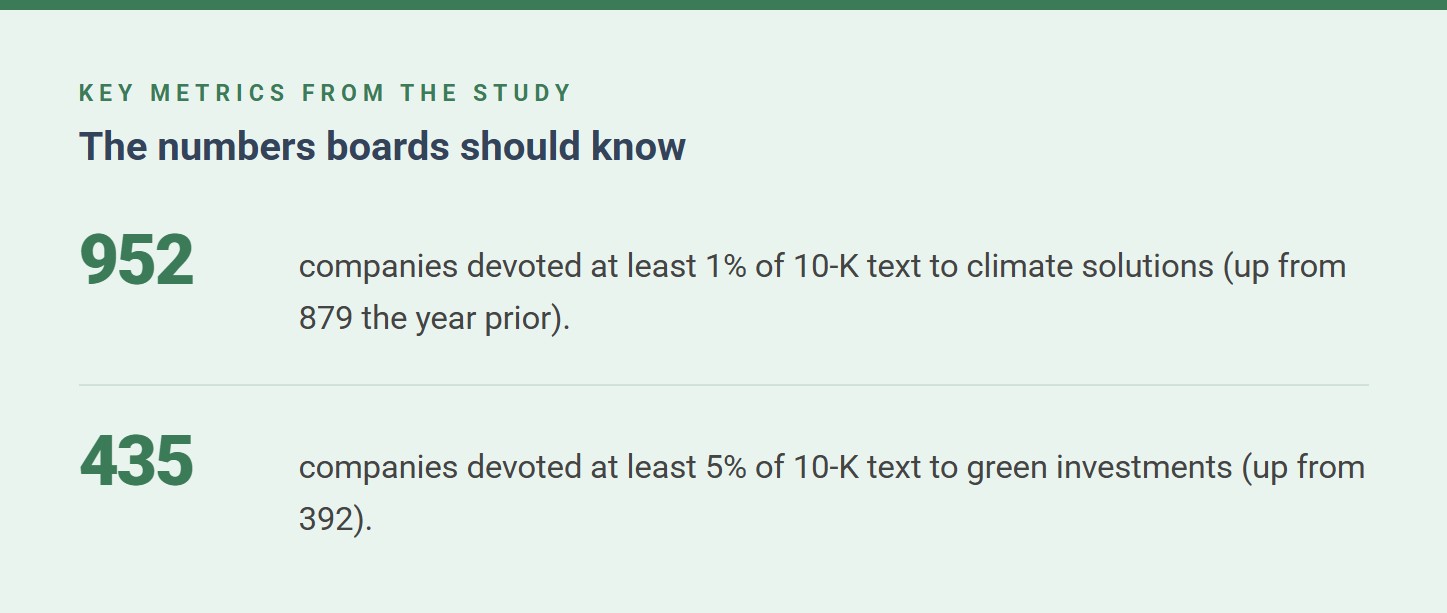

The team analysed 1,918 climate-relevant firms’ 10-K filings (regulated annual reports). Using AI, they measured how much of a company’s disclosure is devoted to climate solutions. Because these filings are tightly regulated, they provide a comparatively consistent window into what companies are prepared to put on record. The research also underpins the BiGS Climate Innovators 100 list- companies with over USD 1 billion in revenue that rank highly on this “climate solution measure.” Unsurprisingly, firms whose core business is climate technology feature prominently, but the list also includes well-known incumbents across autos, chemicals, aviation, utilities, and energy- highlighting that climate solutions are no longer confined to “pure-play” green companies.

The research also underpins the BiGS Climate Innovators 100 list- companies with over USD 1 billion in revenue that rank highly on this “climate solution measure.” Unsurprisingly, firms whose core business is climate technology feature prominently, but the list also includes well-known incumbents across autos, chemicals, aviation, utilities, and energy- highlighting that climate solutions are no longer confined to “pure-play” green companies.

The business case is getting clearer.

One of the most important signals for boards: climate solutions are increasingly framed as growth and competitiveness, not just compliance or reputation. This aligns with the broader economics: renewable power costs have fallen sharply, and many new renewable projects are now cheaper than fossil alternatives in large parts of the world. As a result, more companies see climate-related investment as a pragmatic move -reducing cost, increasing resilience, and opening new markets.What APAC leaders should take from this

For APAC clients, the lesson is not “copy the U.S.”; it’s this: – even in uncertain policy environments, companies that treat climate solutions as a strategy and capability build are pulling ahead. That has three implications:- Disclosure is moving toward decision-grade evidence. Stakeholders are looking for proof points: capex allocation, product innovation, operational milestones, governance incentives, and risk controls; not just targets.

- Transition advantage is becoming operational. Firms are embedding climate considerations into procurement, energy strategy, product design, and financing, creating defensible cost and resilience advantages.

- Policy still matters, but it’s not the only lever. The winners are building optionality: scenarios, modular investment plans, and partnerships that can scale with (or despite) policy swings.

Three practical actions for 2026

- Map “climate solutions” to your profit engines: where is the growth, margin, resilience, or cost case?

- Upgrade governance signals: link leadership incentives to measurable outcomes, not just narratives.

- Stress-test your transition portfolio: identify what survives under weaker incentives and where partnerships or financing can bridge gaps.