The Variable Capital Company (VCC) is Singapore’s newest and perhaps most innovative fund vehicle to date, was announced in October 2018. After significant anticipation, the Singapore Variable Capital Company Act (VCC Act) was officially launched on January 15, 2020 by the Monetary Authority of Singapore (MAS), and the Accounting and Corporate Regulatory Authority (ACRA).

The VCC is intended to bring Singapore to the forefront of global investment services, allowing for almost unrivaled flexibility in both distributions and return on investment.

What is a Variable Capital Company (VCC)?

A VCC is the new legal structure providing for investment funds to be domiciled in Singapore. Its aim is to provide an appealing alternative to existing fund/collective investment schemes (CIS), such as unit trusts, partnerships, corporations, etc.

ACRA administers the VCC Act and subsidiary legislation, with all VCCs required to be overseen by a Permissible Fund Manager. The responsibility for anti-money laundering and countering the financing of terrorism obligations of VCCs falls within the jurisdiction of the Monetary Authority of Singapore (MAS).

Most notably, a VCC is allowed to be set up as a stand alone VCC for a single fund, or as an umbrella VCC with multiple sub-funds.

A VCC can be used as a traditional or alternative fund strategy, either in open-ended or close-ended forms.

While a VCC will have the added diversity of having funds within a fund, in terms of tax, it will still be treated as a regular Singapore company.

Foreign investment funds can be (and are encouraged) to be redomiciled in Singapore as a VCC to enjoy its many benefits.

Components of a VCC

- Governed by the VCC Act of 2018.

- Is able to redeem shares and pay dividends using its net assets. Compared to a traditional corporate fund, this allows a VCC to be agile in its distributions and return of capital.

- It is not required to hold annual general meetings with shareholders.

- It can keep only a private register of shareholders.

- It can use ASC Standard or IFRS, US GAAP, except for VCC offered to retail investors which must use RAP7.

- While it may change in the future, currently it can only be used as:

- traditional or alternative funds.

- retail or restricted funds.

- the standalone fund, or an umbrella entity with multiple sub-funds with segregated assets and liabilities.

- Regulated by the Accounting and Corporate Regulatory Authority (ACRA) for administration objectives, and the Monetary Authority of Singapore (MAS), for the purposes of Anti-Money Laundering/Countering the Financing of Terrorism (AML/CFT) purposes.

- Must appoint a fund management company (FMC) that is registered or licensed with MAS, or is a current exempt private financial service provider in Singapore.

- Must meet the mandatory VCC criteria:

- Needs to apply for the name first before actual incorporation filing. VCC Name application is S$15.

- The suffix of the VCC entity ends with ‘VCC’.

- Preset business SSIC code 64300 — trusts, funds and similar financial entities (e.g. Collective Portfolio Investment Funds [Excluding those with rental income]).

- At least one director must be ordinarily resident in Singapore.

- At least one director (who may be the same person as in d. above) must be either a director or a qualified representative of the manager of the proposed VCC.

- Require one company secretary (like a Pte. Ltd.).

- Min one subscriber (can be either local individual, local corporate entity, or foreign individual/corporate entity).

- Requires a local registered address.

- Requires at incorporation stage to have an FYE formed during incorporation.

- Application for incorporation of VCC fee is S$8000 payable to ACRA.

- Each registration of a VCC sub fund is S$400.

- Must meet Singapore regulatory compliance:

- One or more of the directors must be a registered representative or director of the FMC.

- All directors must be fit and proper individuals.

- Maintain compliance with AML/CFT requirements, however, this can be outsourced to the FMC or other registered and licensed financial institutions in Singapore.

How the VCC Will Be a Game Changer

Singapore to Become a Global Hub for Venture Capital (VC) and Private Equity (PE) Funds

Singapore’s venture capital (VC) ecosystem has steadily matured over the years and is now globally recognised as one of the leading VC hubs, especially within Southeast Asia. With approximately 4,000 technology startups (including 31 unicorns based in Singapore) and 200 incubators choosing Singapore as their home, the city-state achieved its highest-ever ranking of eighth place in The Global Startup Ecosystem Report 2023. This ranking marks Singapore’s second-highest position in Asia, following Beijing at seventh. Moreover, Singapore is among the top 15 countries in the world for ease of securing funding and secured the seventh spot in the Global Innovation Index 2022.

Singapore continues to serve as a central hub for global private equity (PE) fund managers seeking opportunities within the Asia-Pacific region (APAC). APAC holds significant importance as an investment destination for international investors aiming to enhance the diversity of their portfolios. Many international fund managers have already established a presence in Singapore and are either expanding their horizons or venturing into new asset classes.

Redomiciliation Made Easy for VCCs

To attract the appropriate levels of interest, and ultimately an investment in the VCC structure, Singapore must make the re-domiciliation process as easy as possible. Favorably, the re-domiciliation of foreign funds (e.g. a British Virgin Island [BVI] protected cell company) to a Singaporean VCC is made simple on two accounts — established infrastructure, and low threshold investment criteria.

Given Singapore’s long standing as a reputable centre for investment, any respected VC and PE funds will already have an existing registered fund manager in Singapore. This makes any transition incredibly simple and efficient from the perspective of time and cost. If the investor does not have a current fund manager in Singapore, there are a myriad of registered and trusted FMCs and exempt private financial institutions that can make the transition relatively seamless.

In terms of re-domiciliation requirements, foreign funds can shift to VCC structure in Singapore if they have positive net assets, and remain creditworthy within 12 months from the date of their VCC application. The only other requirements are to meet the mandatory Singapore company criteria and Singapore regulatory compliance which are both world-renowned for their lack of bureaucracy and red tape.

Benefits of The VCC

Benefits of the VCC for Fund Managers

Benefits of the VCC for Fund Managers

The VCC structure will bring much-needed flexibility to investment possibilities for Fund Managers in Singapore. This will allow for greater efficiencies both in terms of taxation and operations that will bring Singapore up to par with its tax haven counterparts, such as Luxembourg and Ireland. In both reputation and reality, the VCC is a massive boon for Singaporean Fund Managers. Specific benefits of the VCC for Fund Managers are:

- The possibility of a VCC having sub-funds, in and of itself makes any Singaporean Fund Manager legitimately competitive with any other Fund Manager in the world.

- If a VCC has sub-funds, each sub-fund’s assets and liabilities can be separate from the other sub-funds within the umbrella VCC. This allows a VCC to be used as an alternative to multiple separate companies, providing protection from liability.

- If a VCC has sub-funds, those sub-funds can share a Board of Directors, as well as use the same service providers (e.g. custodian, administrator, etc.), creating considerable savings in operations. This works well as both a sales pitch to the investor from the Fund Manager, as well as time and cost saving tool for said Fund Manager.

- If a VCC acquires another VCC, that original VCC can use the customer due to diligence research already done by the acquired VCC. It is of course up to the VCC doing the acquisition to decide if they have any doubts about said due diligence. Ultimately though, this saves substantial time and money in performing their own due diligence.

- The combination of a VCC structure combined with Singapore having access to 90 tax treaties (second only to the United Kingdom), is a very appealing package to present to investors. That is a truly wide range of markets that can enjoy a double taxation agreement from their VCC investments.

- A VCC is not burdened by the usual capital requirements of a Singapore company as an open-end fund. This provides a low barrier to entry, as well as a low threshold for the operation which should make for an attractive pitch to investors.

- Income from VCC funds may be tax-free if they qualify for the Enhanced Tier Fund (ETF) Scheme for which the main criteria are:

- The VCC fund must have a minimum fund size of S$50 million at the time of application

- The fund must have an annual local business spend of at least S$200,000.

The criteria are measured at the umbrella level, so the sub-funds can combine to qualify for those amounts rather than needing to have each sub-fund be at least S$50 million and spend at least S$200,000.

- Income from VCC funds may be tax free if they qualify for the Singapore Resident Fund (SRF) Scheme:

- The fund must have an annual (not necessarily local) business spend of at least S$200,000.

The criteria is measured at the umbrella level, so the sub-funds can combine to qualify for those amounts rather than needing to have each sub-fund spend at least S$200,000.

- While an Annual General Meeting (AGM) is required in principle, a VCC does not need to hold an AGM if the directors give 60 days’ notice, and all persons entitled receive the appropriate paperwork. If a fund manager has foreign clients who wish to keep things hands-off/passive, this reduction of administration required would be an excellent sales tool.

- Fund Managers will be incentivised by the Financial Sector Incentive Fund Management Scheme, with its 10% concessionary tax rate, providing even more motivation to make VCCs a strong part of their portfolios.

- Fund Managers will be allowed to delegate fund management to a registered third party within Singapore, provided that they maintain overall responsibility for the outsourced fund. This will allow fund managers to focus on new portfolio growth.

- If an offshore fund re-domiciles to Singapore, that means less waking up in the middle of the night for fund managers to deal with directors and service providers in other time zones.

Benefits of the VCC for Local Fund Service Providers

Benefits of the VCC for Local Fund Service Providers

For Singapore fund service providers that have traditionally serviced unit trusts, private companies limited by shares, and/or limited partnerships for open-end or closed-end funds, the VCC structure boasts a range of benefits.

- Singapore has held its own remarkably well on the world’s investment stage, but the addition of the VCC structure will take fund service provider revenue to the next level. With a new and powerful tool in their arsenals, Singapore fund service providers should expect to see substantial increases in business inflow as investors once again pay attention to Singapore as a global investment hub.

- All VCCs can only be launched by a Singapore based regulated fund manager — there will be no foreign competition to interfere or challenge this new revenue stream.

- If a VCC has sub-funds, those sub-funds can share a Board of Directors, as well as use the same service providers (e.g. custodian, administrator, etc.) which provide substantial operational efficiencies for local fund service providers.

- If a VCC has sub-funds, this allows a VCC to be used as an alternative to multiple separate companies, which provide further administration efficiencies for fund service providers.

- Forward-thinking funds service providers may, in fact, re-domicile their existing offshore funds as VCCs in Singapore, to reap the very same rewards they are pitching to their clients. Not only does this make good business and operational sense, but it also shows clients how much they value the Singapore VCC structure. Beyond this, an internal shift to a VCC structure would help reduce the doubling up of regulatory upkeep, such as anti-money laundering compliance for a fund service provider.

- If a VCC acquires another VCC, that original VCC can use the customer due to diligence research already done by the acquired VCC. Yet another cost-efficiency afforded to local fund service providers by the VCC.

- If the VCC chooses to dispense with AGM/s, that will save local fund service providers significant time and money in administration and preparation.

- VCC fund management can be delegated to registered third parties, as long as the original fund service provider maintains overall responsibility including conflict of risk mitigation. This will allow local fund service providers to pass on administrative duties and in turn, allowing more resources to be assigned to continually bringing in new business.

Benefits of the VCC for Investors

Benefits of the VCC for Investors

Ultimately the VCC is designed to be as attractive as possible for investors from around the world. To do this the VCC has had to be both robust and flexible in its structure. Let’s have a look at the main benefits of the VCC for investors.

- Income from eligible VCC funds may be tax-free if they qualify for the Enhanced Tier Fund Scheme or the Singapore Resident Fund Scheme.

- A VCC is a corporate/legal entity, this means a VCC is able to act for and on behalf of itself without the need to appoint a trustee, offering much more freedom than a unit trust or similar entities.

- A VCC is able to issue and redeem shares without having to get shareholders’ approval. This allows investors to exit their investments as they wish, providing much-needed flexibility.

- If required, a VCC can issue dividends using its capital. This is a substantial advantage over companies under the Companies Act that have restrictions on capital reduction, and can only issue dividends out of profits.

- A VCC is an excellent option for investors seeking anonymity, as the register of a VCC’s shareholders does not need to be made public. This should be of great interest to those investors (e.g. ultra-high net worth individuals) who desire discretion.

- While an AGM is required in principle, a VCC does not need to hold an AGM if it chooses.. For passive foreign investors, this would be of huge convenience. With Singapore’s already excellent reputation for corporate governance, investors can be very comfortable with their hands-off approach.

- All sub-funds are insulated from one another, which ensures a poorly performing or insolvent sub-fund cannot adversely affect other sub-funds. This should provide peace of mind for even the most cautious investor.

- If a VCC has sub-funds, those sub-funds can share a Board of Directors, as well as use the same service providers (e.g. custodian, administrator, etc.), passing down those savings to the investors, making a VCC extremely cost-efficient.

- Because VCC can have a single shareholder or hold just a single asset, it can be used as part of a master-feeder structure for favorable pass-through tax treatment as well as economies of scale.

Benefits of the VCC for Singapore

Benefits of the VCC for Singapore

Let’s have a look at what specifically the introduction of the VCC will do to help the country of Singapore as a whole.

- The VCC will help take a greater share of the overall value chain of fund management, building on Singapore’s global reputation in the fund servicing space.

- Singapore should expect a dramatic influx of investment once the VCC attracts funds away from the likes of Dublin, Cayman Islands, and Luxembourg — all traditionally fierce competitors in fund management space.

- This influx of investment from offshore should foster unprecedented economic stability for Singapore, and build the foundations of a prosperous future for its citizens.

- It’s estimated that the VCC will introduce over 1,000 new jobs in Singapore both inside and outside of fund management service providers. “Beyond fund managers, the VCC framework will create new business opportunities for lawyers, accountants, tax advisers, fund administrators and custodians in Singapore,” Ms Indranee said at the passing of the VCC act.

Tax Incentives and Requirements

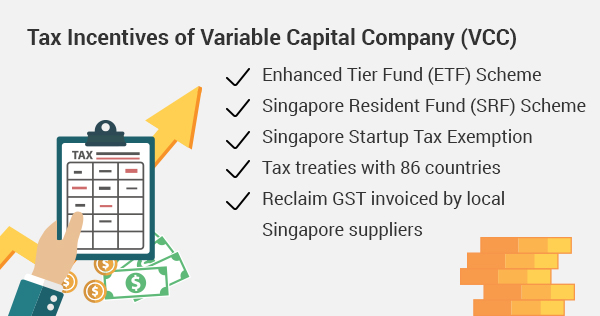

Tax Incentives of VCC

Already well regarded for its generous tax conditions, Singapore has created the VCC in that same vein, and investors will be assured of a wide range of tax incentives.

- Tax incentives are carried over from sections 13R and 13x to VCCs. This means that income from VCC funds may be tax free if they qualify for the Enhanced Tier Fund (ETF) Scheme for which the main criteria are:

- The VCC fund must have a minimum fund size of S$50 million at the time of application

- The fund must have an annual local business spend of at least S$200,000.

The criteria is measured at the umbrella level, so the sub-funds can combine to qualify for those amounts.

- Tax incentives are carried over from sections 13R and 13x to VCCs. This means that income from VCC funds may be tax free if they qualify for the or the Singapore Resident Fund (SRF) Scheme:

- The fund must have an annual (not necessarily local) business spend of at least S$200,000.

The criteria is measured at the umbrella level, so the sub-funds can combine to qualify for that S$200,000.

- If a VCC can meet the appropriate criteria, it can qualify for the Singapore Startup Tax Exemption for the first three years from its incorporation date. This will allow the VCC to be exempted from any tax on the first S$100,000 of the normal chargeable income, and up to 50% of tax on the next S$200,000 normal chargeable income.

- VCCs will enjoy the existing tax treaties with 90 countries, in some cases completely eliminating the risk of double taxation.

- As with other current Singapore investment vehicles, eligible VCCs will enjoy GST remission. VCCs will be able to reclaim GST invoiced by local Singapore suppliers.

- There is potential flexibility for US check the box rules with each sub-fund within an umbrella VCC.

Tax Requirements

As is the norm for all investment vehicles in Singapore, the tax requirements are both transparent and free from red tape. Let’s have a look at the tax obligations of the new VCC fund structure.

- A VCC will be taxed as a single entity at the umbrella level and a single corporate income tax return can be filed with the Inland Revenue Authority of Singapore (IRAS) for the entire umbrella fund including all sub-funds.

- If a VCC has sub-funds, tax residence will be treated from the VCC umbrella level

- However, tax deductions and allowances will be applied at the sub-fund level, and the resulting chargeable income of each sub-fund will then form the total chargeable income of the umbrella.

- A VCC will perform its own GST registration, accounting and reporting on behalf of its sub-funds

- Each sub-fund of a VCC is required to evaluate its GST liability on the value of taxable supplies made.

- The collection of GST will be undertaken at the VCC’s sub-fund level based on the GST returns filed by the GST-registered sub-funds.

- Stamp duty will be applied at the sub-fund level.

Singapore Comparison with Other Tax Haven Countries

One of the main priorities of the VCC corporate structure is to not only bring Singapore into line with other renowned tax haven countries, but to provide genuine competitive advantages. We take a look at a summary of each of these competing tax havens and finally assess where Singapore sits among them with the introduction of the VCC.

Summary of Hong Kong

Summary of Hong Kong

Long known as a gateway to the East, Hong Kong emerged from its British colonisation to be a strong investment player in the Asian region. Hong Kong has attracted substantial global investment with its low tax across the board, as well as no tax on dividends and other capital gains.

Known as a ‘hands off’ market in terms of regulation, Hong Kong has so far resisted calls to open a financial services sector for oversight of the industry. Paired with a reputation for providing secrecy for its investors, Hong Kong has become an attractive option for many.

In July, 2018, Hong Kong introduced that Open-ended Fund Company (OFC) structure, which is similar to Singapore’s VCC in that it can hold sub-funds under a corporate structure. Investors who seek close ties with mainland China will find the OFC structure attractive.

While now a Special Administrative Region (SAR) of China, Hong Kong carries on with its British common law legal system until 2047. However, recent political unrest has raised significant questions in terms of economic security, and China’s interference in the market.

Summary of Australia

Summary of Australia

While not traditionally known as a tax haven, Australia has developed a mature funds market largely based off its national compulsory retirement savings scheme. Known as the Superannuation System, its funds currently total over AU$2.7 trillion. Australia’s overall fund management industry is the biggest in the Asia-Pacifc region.

The Australian Government has been largely open to the prospect of foreign fund management services operating within the Superannuation System to manage funds — within the forms of open-ended and closed-ended investment vehicles, as well as alternative investment options.

Australia’s Corporate Collective Investment Vehicle (CCIV) is one such alternative structure that has been introduced to attract foreign interest, however it has yet to be enacted. It is Australia’s first foray into investment vehicles that allow sub-funds.

Summary of Luxembourg

Summary of Luxembourg

Arguably the world’s most notable tax haven, Luxembourg has been offering tax haven status since the 1970s. Since then, Luxembourg’s finance industry has grown to make up more than 35% of Luxembourg’s GDP. It is Europe’s largest investment fund centre, and the second largest investment fund centre in the world.

With reliable political and economic stability, Luxembourg’s government has traditionally provided an attractive environment for both confidentiality and asset protection. While it’s aggregate corporate tax rate of 24.94% is not particularly outstanding, Luxembourg still offers attractive options such as profit funneling charged at a rate of 1%, and no withholding tax on dividends and other capital gains.

Luxembourg’s version of the VCC is known as the SICAV (société d’investissement à capital variable). As a member of the European Union (EU), Luxembourg also offers all of the benefits of full access to the EU market.

Summary of Cayman Islands

Summary of Cayman Islands

Almost synonymous with the term ‘tax haven’ the Cayman Islands are what even non-investors think of when offshore accounts are mentioned. A small British territory (following English common law), the Cayman Islands are 4,500 miles from the United Kingdom, and about an hour-long flight from Miami. It has been known as a centre for profit funneling as early as the 1960s.

The Cayman Islands have of late made an effort to rid itself of the tax haven moniker, and instill a more reputable image in the minds of investors. It does after all boast a stable political and economic environment, and has reportedly attracted around 85% of the world’s hedge fund investments.

With no official corporate tax rate (although in reality works out to about 13%), the Cayman Islands offers an extremely flexible and versatile range of investment vehicles, including their Cayman segregated portfolio company (SPC), which is most like Singapore’s VCC.

Singapore VCC Equivalence

With the benefit of learning from other markets, the VCC structure has been able to take the best from other investment vehicles, to create what we believe to be a superior investment option. If pushed to choose a competing fund that is the most similar however, we would say the Cayman Islands’ SPC structure would come close.

The VCC offers all of the flexibility of an SPC fund, however it should be faster, easier and less expensive to open and operate. This is in part due to the fact that most regulatory requirements have already been taken care of by the Singapore fund management companies, saving time and money.

Singapore also allows everything to be done within one central area of Singapore, as opposed to the Cayman Island, where most processes are done offshore which will save both investors and fund managers substantial costs.

Singapore arguably also enjoys a more stable climate both economically and operationally than the Cayman Islands, so we expect this will play well to investors who value that reassurance.

Comparison with Competing Structures

Framework

Legal Framework

| Singapore Authorised VCC |

Singapore Variable Capital Companies Act 2018 — Enactment date to be confirmed |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Code on Open-Ended Fund Companies 2018 — Enacted |

| HK Private OFC |

| Australia Corporate CIV |

Corporations Act (Cth) 2001 — Enacted |

| Luxembourg SICAR (SICAV) |

Law of 15 Jun 2004 Relating to the Investment of Company in Risk Capital (SICAR Law) — Enacted |

| Luxembourg SIF (SICAV) |

Law of 13 February 2007

Relating to Specialised Investment Funds (SIF Law) — Enacted |

| Luxembourg RAIF (SICAV) |

Luxembourg Law of 23 Jul 2016 (RAIF law) — Enacted |

| Cayman Islands Segregated Portfolio Company (SPC) |

Mutual Funds Law (2019 revision) — Enacted |

Judicial System

| Singapore Authorised VCC |

Common Law |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Common Law |

| HK Private OFC |

| Australia Corporate CIV |

Common Law |

| Luxembourg SICAR (SICAV) |

Civil Law |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Common Law |

Regulatory Authority

| Singapore Authorised VCC |

MAS/ACRA |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

SFC |

| HK Private OFC |

| Australia Corporate CIV |

ASIC |

| Luxembourg SICAR (SICAV) |

CSSF |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

CIMA |

Types of Securities

| Singapore Authorised VCC |

Shares, debentures |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Shares |

| HK Private OFC |

| Australia Corporate CIV |

Shares, debentures |

| Luxembourg SICAR (SICAV) |

Shares, debt |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Shares, debt |

Governance

Director requirement

| Singapore Authorised VCC |

3 directors required |

| Singapore Restricted/Exempt VCC |

1 executive director and at least 1 independent director |

| Hong Kong HK Public OFC |

2 directors required |

| HK Private OFC |

| Australia Corporate CIV |

1 corporate director required |

| Luxembourg SICAR (SICAV) |

2 directors required |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

1 director required |

Director Residence Requirement

| Singapore Authorised VCC |

1 director must be resident in Singapore |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Directors do not need to be residents, but will need to be approved by the SFC and have local process agent in Hong Kong |

| HK Private OFC |

| Australia Corporate CIV |

Corporate director must be a public company holding an Australian financial services (AFS) licence |

| Luxembourg SICAR (SICAV) |

Directors do not need to be resident in Luxembourg |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Directors do not need to be resident in the Cayman Islands |

Director Independence from Fund Manager Requirements

| Singapore Authorised VCC |

Directors need to be independent from fund manager |

| Singapore Restricted/Exempt VCC |

Directors are not required to be independent from fund manager |

| Hong Kong HK Public OFC |

Directors are not required to be independent from fund manager, but 1 director must be independent of the custodian |

| HK Private OFC |

| Australia Corporate CIV |

At least half of the corporate director’s board must be external directors (only applies to public funds) |

| Luxembourg SICAR (SICAV) |

All directors are not required to be independent from fund manager, but CSSF expects the majority of directors to be independent of the fund manager |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Directors are not required to be independent from fund manager |

Fund Manager Director Requirements

| Singapore Authorised VCC |

Fund manager directors are required |

| Singapore Restricted/Exempt VCC |

At least one fund manager director is required |

| Hong Kong HK Public OFC |

Fund manager directors are not required, but 1 director must be independent of the custodian |

| HK Private OFC |

| Australia Corporate CIV |

Fund manager directors are not required |

| Luxembourg SICAR (SICAV) |

Fund manager directors are not required |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Fund manager directors are not required |

Fund Management

Fund Manager Location

| Singapore Authorised VCC |

Singapore |

| Singapore Restricted/Exempt VCC |

Singapore only |

| Hong Kong HK Public OFC |

Hong Kong |

| HK Private OFC |

| Australia Corporate CIV |

Australia |

| Luxembourg SICAR (SICAV) |

Not Alternative Investment Fund Managers (AIFM) Law compliant: any location; delegated portfolio management must in principle be a regulated entity

AIFM Law compliant: must be based in EU but portfolio management can in principle only be delegated to a regulated entity anywhere |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

Must be based in EU but portfolio management can be delegated anywhere to a regulated entity |

| Cayman Islands Segregated Portfolio Company (SPC) |

Fund manager can be anywhere |

Minimum Capital

| Singapore Authorised VCC |

No minimum capital required |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

No minimum capital required |

| HK Private OFC |

| Australia Corporate CIV |

No minimum capital required |

| Luxembourg SICAR (SICAV) |

Minimum capital of EUR 1 million required within 12 months following application approval |

| Luxembourg SIF (SICAV) |

Minimum capital of EUR 1.25 million required within 12 months following application approval |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

No minimum capital required |

Reports and Registers

Financial Statements at Sub-Fund Level

| Singapore Authorised VCC |

Financial statements can be done at sub-fund level |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Financial statements can be done at sub-fund level |

| HK Private OFC |

| Australia Corporate CIV |

Financial statements can be done at sub-fund level |

| Luxembourg SICAR (SICAV) |

Financial statements can be done at sub-fund level |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Financial statements can be done at sub-fund level |

Financial Reporting Standards

| Singapore Authorised VCC |

Presentation as per the Code of Collective Investment Schemes RAP7 |

| Singapore Restricted/Exempt VCC |

SFRS, IFRS, US GAAP |

| Hong Kong HK Public OFC |

An OFC may apply HKFRS or IFRS. The financial statements must include the information set out in Chapter 9.4 of the Code on Open-ended Fund Companies. Other accounting standards will be acceptable where appropriate for the OFC. |

| HK Private OFC |

| Australia Corporate CIV |

FRS, Australian GAAP/AASB |

| Luxembourg SICAR (SICAV) |

IFRS, Lux GAAP |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Any GAAP |

Public Financial Statements

| Singapore Authorised VCC |

Financial statements are not public |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Financial statements are not public |

| HK Private OFC |

| Australia Corporate CIV |

Financial statements lodged with ASIC |

| Luxembourg SICAR (SICAV) |

Financial statements are not public. However, it is filed with the register of commerce in Luxembourg which is public |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Financial statements are not public |

Financial Statements Submitted to Which Authority

| Singapore Authorised VCC |

ACRA only, not publicly available |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

SFC |

| HK Private OFC |

| Australia Corporate CIV |

Only public funds have to lodge financial statements with ASIC |

| Luxembourg SICAR (SICAV) |

CSSF and Register of Commerce |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

Register of Commerce |

| Cayman Islands Segregated Portfolio Company (SPC) |

CIMA |

Public Shareholder Lists

| Singapore Authorised VCC |

Shareholder lists are not publicly available |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Shareholder lists are not publicly available |

| HK Private OFC |

| Australia Corporate CIV |

Shareholder lists are not publicly available |

| Luxembourg SICAR (SICAV) |

No, with the exception of the effective beneficial owner |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Shareholder lists are not publicly available |

Check the Box and Redomiciliation

Check the Box Election?

| Singapore Authorised VCC |

Check the box election is available |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Check the box election is not mentioned |

| HK Private OFC |

| Australia Corporate CIV |

No, Public Limited Company |

| Luxembourg SICAR (SICAV) |

Check the box election is available, depending on the legal form |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Check the box election is available |

Allowance of Redomiciliation

| Singapore Authorised VCC |

Yes, re-domiciliation is available |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

No, migration of the corporate fund to Hong Kong may in practice be conducted by alternative means, including for example by way of an asset transfer or share swap. No restriction on the restructuring of unit trusts into OFCs provided that the relevant requirements for establishing an OFC under the Amendment Ordinance, the OFC Rules and OFC Code are complied with and that such restructuring could be conducted in accordance with the unit trust’s constitutive documents. |

| HK Private OFC |

| Australia Corporate CIV |

CCIV is required to be a company limited by shares |

| Luxembourg SICAR (SICAV) |

Yes, re-domiciliation is available |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Yes, re-domiciliation is available |

Tax Treaties

Number of tax treaties in the jurisdiction

| Singapore Authorised VCC |

90 |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

37 |

| HK Private OFC |

| Australia Corporate CIV |

44 |

| Luxembourg SICAR (SICAV) |

83 |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

NIL |

Can the Fund Access the Tax Treaties?

| Singapore Authorised VCC |

Yes, it can access the tax treaties |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Yes, it can access the tax treaties, if it meets certain criteria |

| HK Private OFC |

| Australia Corporate CIV |

Generally yes, it can access the tax treaties, but it depends on the country |

| Luxembourg SICAR (SICAV) |

Limited |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

N/A |

Service Provider Requirements

Company Secretary

| Singapore Authorised VCC |

Yes |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

No company secretary is required |

| HK Private OFC |

| Australia Corporate CIV |

No company secretary is required |

| Luxembourg SICAR (SICAV) |

No company secretary is required |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

No company secretary is required, but must have a registered office in Cayman Islands |

Administrator

| Singapore Authorised VCC |

Yes, but only via the tax incentives |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

No requirement for appointment of administrator |

| HK Private OFC |

| Australia Corporate CIV |

Not yet known |

| Luxembourg SICAR (SICAV) |

Yes |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Yes, but only for Administered funds |

Custodian

| Singapore Authorised VCC |

Yes, should meet the same eligibility requirements as set out in the Code of Collective Investments Schemes |

| Singapore Restricted/Exempt VCC |

Yes, Singapore registered Custodian Not for private equity and real estate funds |

| Hong Kong HK Public OFC |

Yes, should meet the same eligibility requirements as set out in the Code on Unit Trusts and Mutual Funds |

| HK Private OFC |

| Australia Corporate CIV |

Yes |

| Luxembourg SICAR (SICAV) |

Yes |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

No |

Auditor

| Singapore Authorised VCC |

Yes |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Yes |

| HK Private OFC |

| Australia Corporate CIV |

Yes, for public funds only |

| Luxembourg SICAR (SICAV) |

Yes |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Yes, for all CIMA registered funds |

Listing, AGM, Cross Sub-Fund Limit

Listing Ability?

| Singapore Authorised VCC |

Yes |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Not mentioned |

| HK Private OFC |

| Australia Corporate CIV |

No, subject to the consideration of the outcomes of consultation |

| Luxembourg SICAR (SICAV) |

Yes |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Yes |

Are Shareholder Meetings Required?

| Singapore Authorised VCC |

Can be dispensed |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Subject to the OFC’s instrument of incorporation |

| HK Private OFC |

| Australia Corporate CIV |

No, if the director passes a resolution |

| Luxembourg SICAR (SICAV) |

Yes, for incorporated entities |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Not required |

Segregation of Assets and Liabilities for Umbrella Fund Legislatively Provided

| Singapore Authorised VCC |

Yes |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Yes |

| HK Private OFC |

| Australia Corporate CIV |

Yes |

| Luxembourg SICAR (SICAV) |

Yes, in the SICAR law |

| Luxembourg SIF (SICAV) |

Yes, in the SIF law |

| Luxembourg RAIF (SICAV) |

Yes, in the RAIF law |

| Cayman Islands Segregated Portfolio Company (SPC) |

Yes |

Cross Sub-Funds Investments

| Singapore Authorised VCC |

Yes |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

No |

| HK Private OFC |

| Australia Corporate CIV |

No, subject to the consideration of the outcomes of consultation |

| Luxembourg SICAR (SICAV) |

No |

| Luxembourg SIF (SICAV) |

Yes, with restrictions |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

Yes, with restrictions |

Are There Cross Sub-Fund Investment Restrictions?

| Singapore Authorised VCC |

No |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

Yes |

| HK Private OFC |

| Australia Corporate CIV |

N/A |

| Luxembourg SICAR (SICAV) |

Yes, with restrictions |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

No, where appropriately structured |

Tax Filing

Tax Returns to Be Filed

| Singapore Authorised VCC |

Yes |

| Singapore Restricted/Exempt VCC |

| Hong Kong HK Public OFC |

No |

| HK Private OFC |

Yes, but only if there is a charge to Hong Kong tax |

| Australia Corporate CIV |

Yes |

| Luxembourg SICAR (SICAV) |

Yes |

| Luxembourg SIF (SICAV) |

| Luxembourg RAIF (SICAV) |

| Cayman Islands Segregated Portfolio Company (SPC) |

No |

Reference Source — The Singapore Variable Capital Company

Conclusion

There is little doubt that the VCC will be a game-changer for investors, fund managers, local fund service providers, and Singapore as a whole. Compared to Singapore’s existing unit trusts, limited partnerships and companies, the VCC will allow for unprecedented flexibility in both distributions and return on investment. It will now be possible to have separate, isolated sub-funds that can share resources. VCCs will be able to issue and redeem shares without shareholders’ approval, and can also issue dividends using its capital.

Add to this a robust, low red tape fund management environment, and as of 2024, Singapore has over 90 global tax treaties, the VCC will catapult Singapore to the forefront of investors’ minds.

While this strong initiative may seem extreme, in actuality, it is really quite measured. The VCC will simply bring Singapore in line with other global investment hubs, all while using a structure that has learned the lessons of growing pains endured by others. From there, Singapore has a fund with all of the advantages, with less of the disadvantages from global competition.

The VCC will be a game-changer for all involved.

We’ve done our utmost to provide you with the most comprehensive information possible in regards to the VCC and what it means to everyone involved. If you have any other questions about the VCC, please do not hesitate to contact us.

Frequently Asked Questions

- A Variable Capital Company (VCC) in Singapore is a corporate structure tailored for investment funds. It allows for flexibility in share issuance and redemptions without shareholder approval, making it suitable for open-ended and closed-ended fund structures. VCCs can be used for various investment strategies and benefit from tax exemptions under Singapore’s fund tax incentive schemes.

Contact Us

Planning to start a Variable Capital Company (VCC) in Singapore?

About the Author

InCorp's content team includes talented copywriters from our regional group and globally. We contribute informative, thought leadership, and market-trending articles to guide aspiring business entrepreneurs to a higher level across the Asia-Pacific region.

More on Business Blogs